Koyo Pulls the Open Banking Card, Announces another Funding Round

FACTS

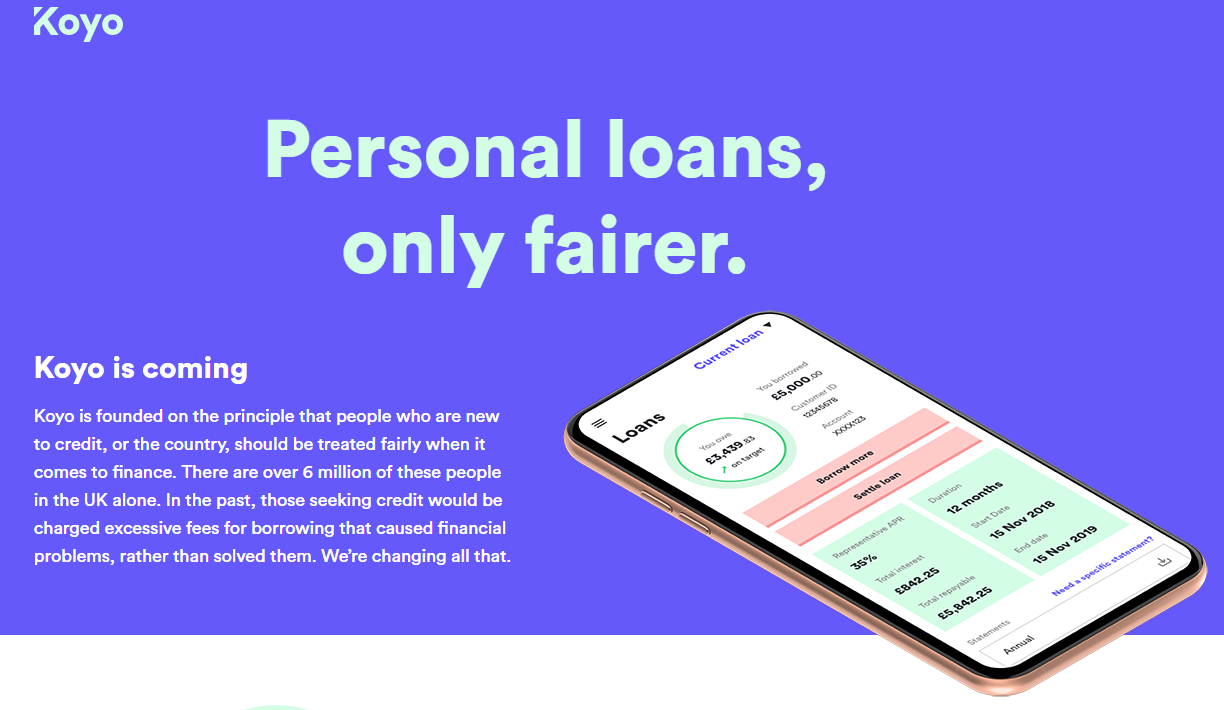

- The British company Koyo announced a $4.9 million funding round. This FinTeh was founded in 2018 and mostly deals with customers without a credit history (e.g.: expats) or poorly addressed by banking institutions.

- Koyo provides them with short-term loans at lower rates (compared to conventional institutions).

- They made the most of Open Banking-entailed opportunities and on their direct access to bank data to build their service. They may then feature customised offers, best suited to specific financial situations.

- Their latest investment will be fuelling their platform scheduled to launch by the end of the year.

CHALLENGES

- Aiming for new customers. Koyo aims for newly arrived customers or people poorly addressed by conventional British institutions (poor credit history), who might not be considered by the main credit rating bureaus (Equifax, Experian, Transunion), i.e.: nearly 6 million people in the UK.

- Analysing financial data to improve credit scoring processes. With access to these customers’ bank accounts, Koyo might more accurately assess their repayment ability, actual income and average spending, using this information instead of typical credit history.

MARKET PERSPECTIVE

- The British banking landscape has been making room for more financial players relying on innovative technologies to provide people with customised products and services best suited to their needs. These players also add flexibility in budget management processes, e.g.: Monzo, Klarna, Starling Bank or Revolut.

- Besides, industry specialists such as Zopa or HSBC with Equifax also aimed at applying Open Banking opportunities to borrowers’ needs.

- In France, more Open Banking-related use cases have seen the day in the credit industry, as no central consumer credit database is available. Younited Credit and Franfinance already bet on account connections to score some of their customers.

- And American Express recently teamed up with Nova Credit to address a similar issue in the US: provide newcomers with access to the credit history they built in their country of origin.